Best Mortgage Lenders of 2025

Summary: Compare the Best Mortgage Lenders of 2025

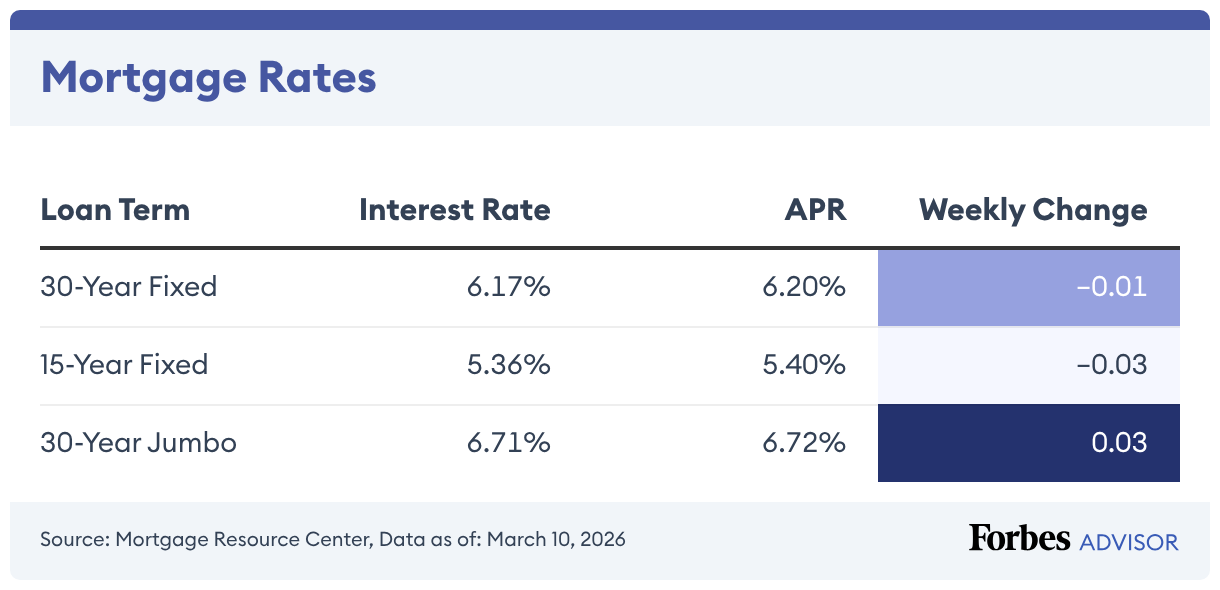

Current Conventional Mortgage Rates

The rates shown here are sourced from the Mortgage Research Center (MRC), which uses standardized parameters—$315,000 for conforming loans and $850,000 for nonconforming loans—when determining rates. These daily rates are calculated assuming a minimum credit score of 740, an 80% loan-to-value (LTV) ratio and a rate lock period ranging from 30 to 60 days.

How To Get a Mortgage

Buying a home is one of the biggest financial decisions you’ll make in your lifetime. Before you apply, take action and follow these five steps:

- Look at your credit. Before applying, comb through your credit report and look for errors you can fix. Keep in mind that conventional mortgages usually require a minimum 620 credit score, while government-backed loans have lower score requirements.

- Pay down debts. Lenders consider how much debt you already have relative to your income. This is your debt-to-income (DTI) ratio. Paying down existing debt can reduce your DTI ratio, which can increase your approval odds and may get you a better rate.

- Prepare paperwork. When you apply for a mortgage, the lender requires copies of some financial documents. Make sure to have your W-2s, tax returns, recent pay stubs and bank statements ready.

- Shop around. Don’t settle for the first mortgage lender you find. Shopping around and comparing lenders could save you money in the form of a better rate or lower fees.

- Get preapproved. Having a mortgage preapproval can show buyers that you’re motivated to buy and how much you can afford. Consider getting mortgage preapprovals from several lenders before home shopping and submitting offers.

Picking a Mortgage Lender

You don’t have to go with the first lender you find. Before applying for a mortgage, compare several lenders to find the best offer for your money. Shopping around can help you find a lender offering the best rates and terms for your financial needs. First, consider our recommendations and make a shortlist of lenders offering the features you’re looking for. For many borrowers, the most important features of a lender to consider are:

- Mortgage rates

- Loan types

- Closing costs and other fees

- Credit score requirements

- Customer service

Calculate Your Mortgage Payments

When researching for a lender, calculate your potential mortgage payments ahead of time to know what terms you can afford. Use our calculator below to simplify the process.

Calculate your mortgage payments by entering your home price, anticipated down payment, interest rate and loan term. If you have additional information about homeowners insurance costs, property taxes, private mortgage insurance (PMI) or HOA fees, select “Show Additional Options” to add those values below. When you’re ready, click “Calculate” to see your monthly payment and estimated payoff date. The amortization schedule shows how your mortgage will be paid down over time and what portion of each payment goes to interest and principal.

Types of Mortgages

There are six common types of mortgages you can use to buy a home. These include conventional, jumbo and nonqualified mortgages (non-QM), as well as government-backed loans from the Federal Housing Administration (FHA), Department of Veterans Affairs (VA) and U.S. Department of Agriculture (USDA).

1. Conventional Mortgage

2. FHA Loan

3. VA Loan

4. Jumbo Mortgage

5. Non-QM Loan

6. USDA Loan

Is 2025 a Good Time for a Mortgage?

Many experts say that the housing market is impossible to time and that the best time to buy a house is when you need one. But because this is the largest purchase that most people make in their lifetime, it’s crucial to be on a solid financial footing before buying. If you’re being cautious about timing, monitoring the housing market may help you determine what financial position you should be in before buying. Check out Forbes Advisor’s Housing Market Forecast for expert analysis of the market and rates.

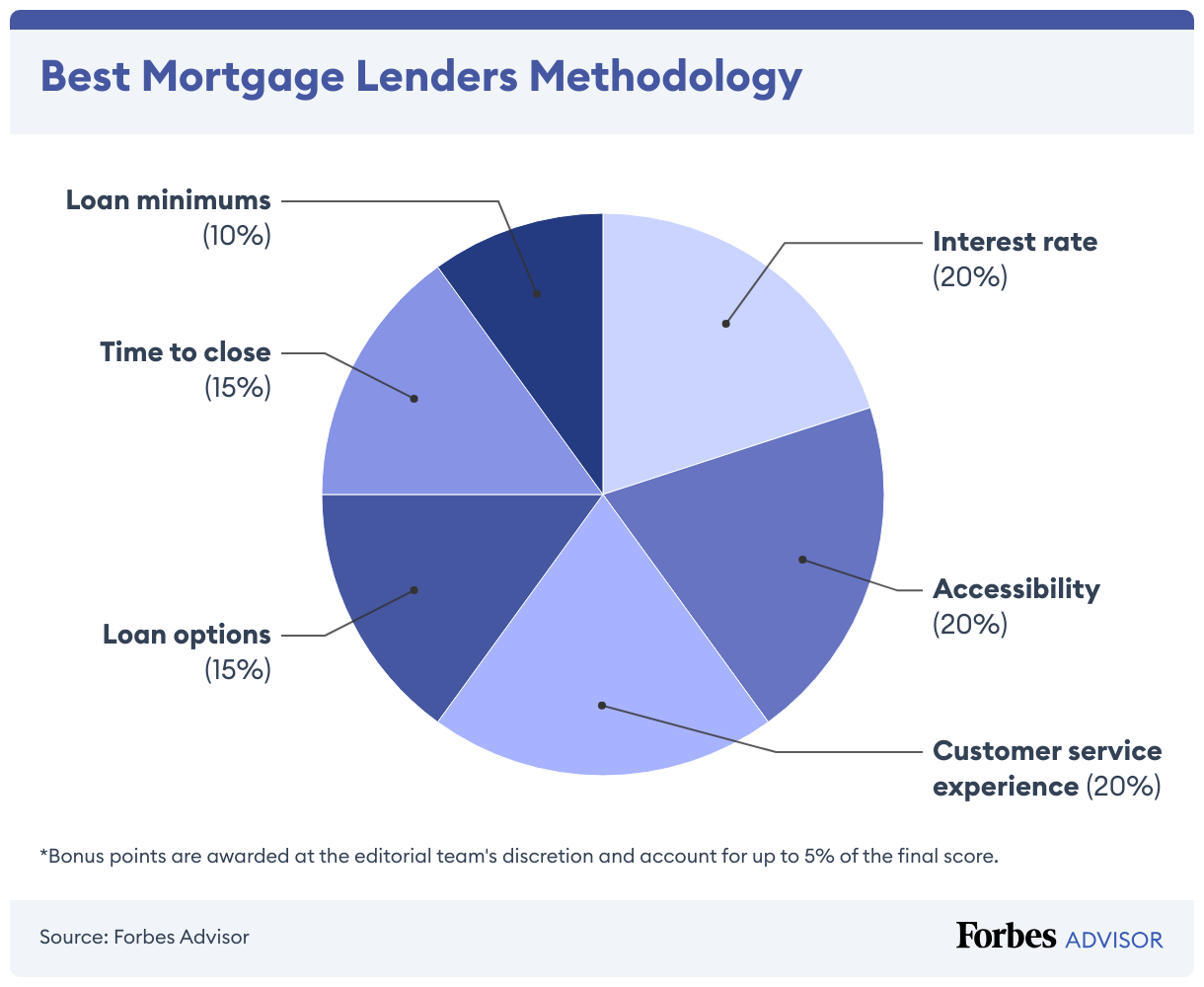

Methodology

Forbes Advisor graded the best mortgage lenders based on features that have a meaningful impact on the cost of a mortgage and a borrower’s experience, including interest rates, loan options, accessibility, closing time and customer service. We award bonus points if a lender offers a specialty mortgage product, rate discount or considers alternative credit data when determining loan eligibility. Our scoring method is broken down as follows:

- Interest rate. 20%

- Accessibility. 20%

- Customer service experience. 20%

- Loan options. 15%

- Time to close. 15%

- Loan minimums. 10%

- Bonus points. Up to 5% of the total score

We chose to focus on these core elements to bring forward lenders that offer the most competitive rates while also providing a satisfactory customer experience accessible to borrowers of all financial backgrounds. We believe this scoring system best reflects consumers’ top priorities when comparison shopping for mortgage lenders. To learn more about our rating and review methodology and editorial process, check out our guide on How Forbes Advisor Reviews Mortgage Lenders.

Frequently Asked Questions (FAQs)

How do I get the best mortgage rate?

Getting your credit as strong as possible is the best way to get a lower mortgage rate. Start by checking your credit score and addressing any problems. It also helps to pay down large debts and maintain on-time payments. Continue to save as much as possible for a down payment because the more you save, the less you have to borrow. Also, check mortgage rates regularly and shop around for lenders.

How much house can I afford?

To find out how much house you can afford, you’ll need to determine your budget. Consider your monthly earnings and spending to see where your money goes. Generally, spend no more than 30% of your gross monthly income on your mortgage. That should also include taxes, insurance and applicable HOA fees. Forbes Advisor’s affordability calculator can help you take the guesswork out of how much you should spend on a house.

What is private mortgage insurance (PMI)?

Private mortgage insurance, also known as PMI, protects the lender in the event that you default on your mortgage. Typically, if you make a down payment of less than 20% of your home’s purchase price, you will be required to pay PMI. How much you’ll pay for this insurance varies and depends on factors that include the size of your down payment and your credit score.

Is it better to get a mortgage from a bank or a lender?

Whether it’s best to get a mortgage from a bank or a lender depends on your refinancing priorities. While banks offer a wider range of services, dedicated mortgage lenders may offer more competitive rates and flexible terms. Likewise, mortgage lenders can have more streamlined applications and online preapproval processes.

Are credit unions better than banks for mortgages?

Credit unions can be better than banks for mortgages, but the best choice depends on your needs and financial situation. Some credit unions offer lower interest rates and fees than traditional banks. Credit unions often offer a more personalized borrowing experience than banks and may be less likely to sell your mortgage to an aggregator like Fannie Mae or Freddie Mac. That said, banks typically offer more mortgage products and have more robust online services.

What happens after you've paid off your mortgage?

After you’ve paid off your mortgage, the lender will record a document to release the lien on your property. The mortgage lender will also send you a notice confirming that the mortgage is paid off, as well as a check for remaining escrow funds. Once your mortgage is paid off, you won’t be able to deduct mortgage interest payments on your taxes, and you’ll need to pay your property taxes directly.

How much money do you need for a down payment?

Typically, you need between 3% and 20% of the purchase price as a down payment on a house. This amount depends on the loan program, as some government-backed loans come with 0% down payments. According to the Mortgage Research Center, the average down payment for first-time homebuyers was 9% in 2024. Lenders typically require private mortgage insurance for down payments less than 20% on conventional mortgages.